RBI’s 2FA Mandate and the Case for Smarter OTP Design

Why RBI's 2FA mandate should also push us to rethink how OTPs are designed - numbers for money, letters for identity.

On 25th September 2025, the Reserve Bank of India announced that from 1 April 2026, all digital payments will require two-factor authentication (2FA).

This is a huge step forward — ensuring that every digital payment, whether through UPI, cards, or wallets, has at least two distinct layers of security, one of which must be dynamic (unique per transaction). RBI has also said that issuers could be liable to compensate customers if they fail to comply, and that cross-border “card-not-present” transactions must follow by October 2026.

Strong regulation. Necessary guardrails. A safer system.

But here’s the catch: technology alone is not enough.

The Problem of Mixed Messages

Back in October 2021, I wrote about how our use of OTPs confuses the very people we’re trying to protect.

We tell our parents, relatives, and friends: “Never share your OTP with anyone.”

At the same time, courier deliveries, service providers, and platforms ask for an OTP to confirm identity.

This inconsistency makes it harder for people to know which OTP is dangerous to share and which is harmless. For a digitally savvy user, it may be a minor inconvenience. For the vulnerable, it can be catastrophic.

The 2021 Proposal: Differentiate OTP Formats

My suggestion then was simple: change the format of OTPs depending on the transaction type.

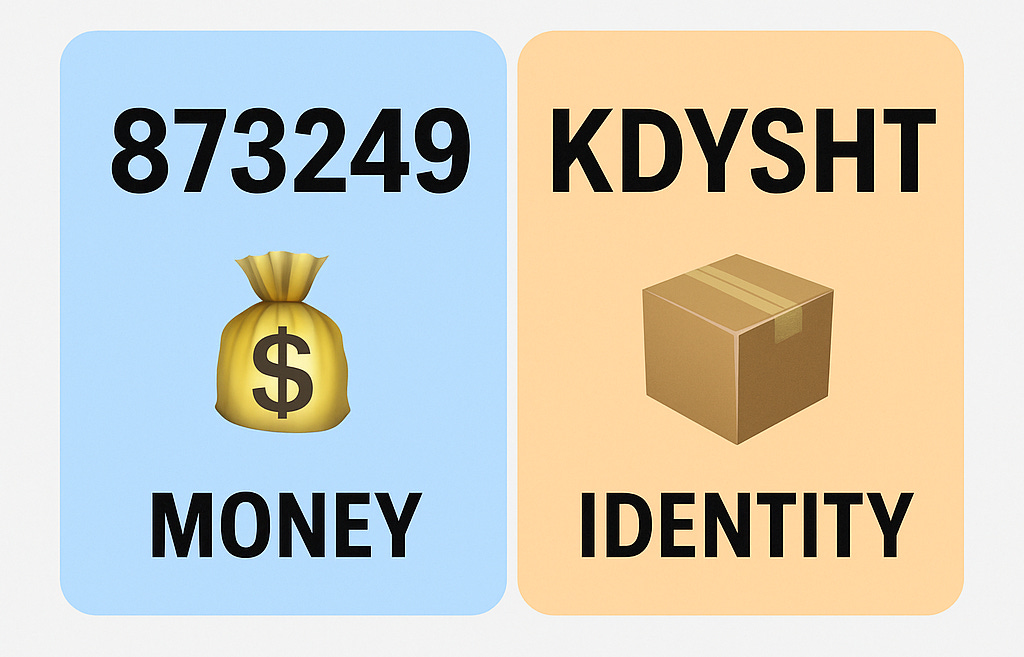

Financial transactions (outgoing payment): Keep OTPs numerical, ideally 6 digits (e.g., 873249).

Non-financial transactions (identity confirmation, deliveries, etc.): Shift OTPs to alphabetical codes, 4–6 letters (e.g., SHYZ or KDYSHT).

That way, the mental model becomes obvious:

Numbers = money moves 💸

Letters = identity proof 📦

No second-guessing. No mixed signals. Just clarity.

Why RBI’s New Directions Make This Urgent

RBI’s 2FA mandate ensures better protection — but as OTPs become more deeply embedded in every transaction, the design of OTPs matters as much as the regulation.

A dynamic factor could mean tokens, app-based prompts, or new forms of OTPs.

But without clear differentiation, users will still be at risk of scams.

Regulators and PSPs should now seize this moment to build a dual OTP standard — not just secure, but understandable.

The Way Forward

It’s time for banks, fintechs, e-commerce players, and regulators to:

Adopt dual-format OTPs (numeric vs. alphabetical).

Communicate clearly and consistently with consumers.

Measure success not only in fraud reduction, but in user confidence.

Because security isn’t just about systems.

It’s about making safety obvious to everyone.

Build This Next.

I write about how products can be better — fixing what’s broken and imagining what’s missing.

If this made you notice something broken or missing, you can subscribe to Build This Next to receive future essays directly.

Every subscription is a vote for building better products.

And if this sparked an idea, take a few seconds to share it — it might help someone else build or see products differently.